Introduction: The Rearview Mirror Fallacy

For over two decades, enterprise fraud management has suffered from a fundamental ontological error: the systematic conflation of realized losses with underlying risk. In boardroom presentations and operational sprint reviews alike, the standard baseline of performance remains a variation of a single line graph—the historical fraud loss rate. When losses drop, teams celebrate their controls; when losses spike, panic ensues, policies tighten, and engineering resources are reallocated to mount a defensive shield.

This reactive loop is a systemic vulnerability. In the context of contemporary risk landscapes, treating realized losses as the definitive proxy for fraud risk is equivalent to navigating an aircraft through heavy cloud cover by looking exclusively at the trailing wake. Realized losses are not risk. Losses are an $n = 1$ historical sample path drawn from a dynamic, multi-dimensional probability distribution. They are a lagging, highly censored, and exceptionally noisy echo of an environmental state that has frequently already mutated by the time the chargeback arrives.

To move past this paradigm, we introduce the Adaptive Quantitative Fraud Management (AQFM) framework. The core insight of AQFM is simple yet profound: Fraud Risk is the latent probability distribution from which loss realizations are drawn. Your risk can dramatically deteriorate while your losses remain temporarily low; conversely, your teams can implement heavy user friction that severely suppresses transaction volume without fundamentally altering your underlying vulnerability surface.

AQFM provides a rigorous, four-part operational methodology—structured around the core verbs Measure, Model, Decide, and Adapt—designed to shift an organization from reactive firefighting to active, distributional engineering. By focusing on shaping the latent risk distribution rather than swatting at historical data points, AQFM establishes a predictable, quantifiable risk discipline.

The Conceptual Bedrock of AQFM

To understand why a new framework is necessary, one must dissect the mathematical disconnect between risk and loss. When a fraud ring discovers a systemic exploit in a fintech platform—such as an undocumented API edge case or a loophole in identity verification—the underlying fraud risk profile spikes instantly. The probability mass of a catastrophic loss event shifts dramatically to the right.

However, the observed losses from this vulnerability will not manifest for days, weeks, or even months. The signal is delayed by financial clearing networks, the consumer reporting lifecycle, and automated dispute timelines. If a risk team measures success purely via a 30-day moving average of realized losses, they are blind to the fact that their platform’s risk topology has completely buckled beneath them. They are operating under the dangerous illusion of safety.

This brings to light the phenomenon of censoring and noise. Realized fraud signals are heavily censored by existing controls. If a system blocks 95% of attempts via a legacy rules engine, the remaining 5% of losses do not reflect the true intent or capability of the adversary; they merely reflect the gaps in that specific line of defense. If the adversary alters their behavior slightly, the system’s brittle rules can fail catastrophically, transforming a flat loss line into an exponential surge overnight.

Furthermore, the common remedy for rising risk—deploying heavy user friction, such as mandatory step-up authentication for all transactions—frequently fails to change the risk profile. Friction often acts as a temporary filter or dampener on transaction velocity. It changes the observed sample path by discouraging both legitimate users and casual fraudsters, but it leaves the systemic structural vulnerabilities completely unaddressed. The moment the friction is dialed back to satisfy commercial conversion goals, the latent risk asserts itself once more. AQFM separates these elements cleanly: friction is a tactical dial; structural distribution shaping is the strategic goal.

The Core Axiom of AQFM

Let L be the stochastic variable representing realized fraud losses, and let ν represent the latent state of environmental fraud risk. Realized losses are generated via a hidden probability density function:

where 𝒞 represents the system’s active controls. Traditional fraud management optimizes for historical realizations of L. AQFM optimizes for the parameters governing the distribution f.

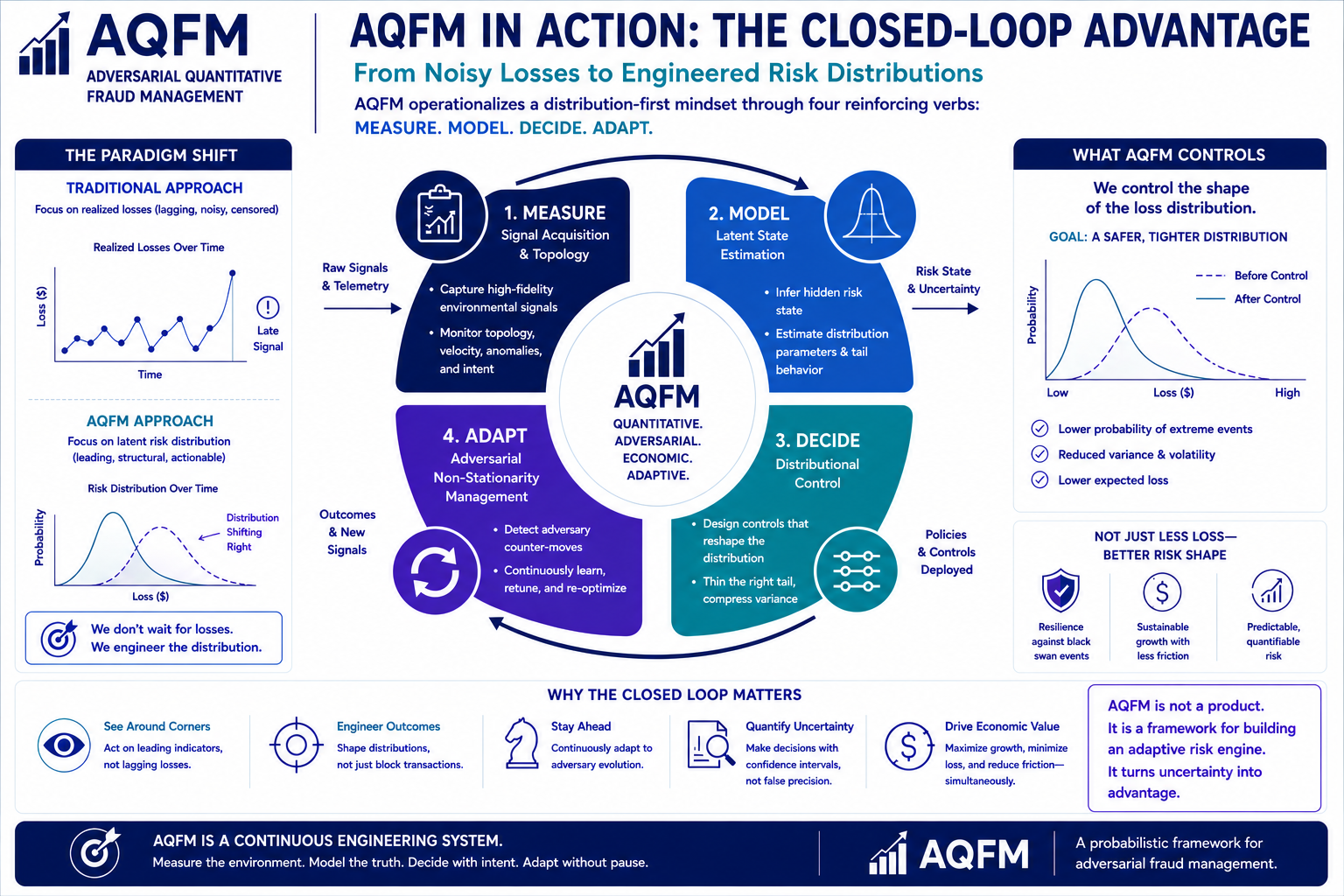

The Four Verbs of AQFM

The AQFM framework operationalizes this philosophy into a continuous, self-reinforcing engineering loop governed by four specific actions: Measure, Model, Decide, and Adapt.

| Verb | Operational Definition | Strategic Focus |

|---|---|---|

| Measure | Signal Acquisition & Environmental Telemetry | Gathering non-loss state variables to map system topology and signal-to-noise ratios. |

| Model | Latent State Estimation | Employing quantitative models to reconstruct the hidden parameters of the unobservable risk PDF. |

| Decide | Distributional Control | Deploying controls and policies designed specifically to compress variance and thin the right tail. |

| Adapt | Adversarial Non-Stationarity Management | Continuous tracking of adversary counter-moves to continuously retune the structural distribution. |

MEASURE: Signal Acquisition & Topology

In traditional risk paradigms, measurement equals counting bodies—aggregating chargebacks, merchant disputes, or confirmed account takeovers. Under AQFM, measurement undergoes a radical transformation. Because realized losses are recognized as lagged and sparse, the Measure phase focuses on capturing the immediate, high-fidelity environmental state variables and system telemetry that reflect the true density of risk.

To measure risk distribution effectively, an architecture must ingest signals that are leading indicators of vulnerability. This includes tracking anomalies in the system’s signal-to-noise ratios, behavioral velocity vectors, device fingerprint distributions, and network routing metadata. For instance, rather than tracking how many accounts were successfully compromised, AQFM measures the mathematical distribution of automated login attempts relative to historical baselines, observing shifts in IP address dispersion and entropy profiles.

Consider a practical scenario: a sudden influx of transactions originates from a newly spun-up block of residential proxy networks. The realized loss metrics show nothing unusual because the accounts are freshly created and have not yet passed the chargeback window. However, the Measure layer of AQFM flags a severe skewness in the device-session distribution. The telemetry indicates that the environment’s state variables have changed. We are no longer observing standard consumer traffic; the variance of the input signal has widened. By measuring the system’s operational topology rather than its historical wreckage, AQFM alerts the enterprise that the probability density function has begun shifting to the right long before the first financial hit occurs.

MODEL: Latent State Estimation

The second pillar of AQFM addresses an inescapable mathematical truth: the true risk distribution is a latent object that cannot be directly observed. You cannot look directly at an incoming payment transaction and see its absolute mathematical truth; you can only observe variables that correlate with its legitimacy. Therefore, risk management must be treated as an inverse problem, where we observe noisy, lagged point realizations and must mathematically back-calculate the parameters of the hidden generative distribution.

This realization invalidates the traditional reliance on simple binary classification machine learning models. A standard model outputs a point-in-time score between 0 and 1, predicting whether a specific transaction is fraud. While useful at an atomic level, a collection of individual binary scores does not equal a structural risk distribution. AQFM demands structural or state-space modeling frameworks—such as Hidden Markov Models (HMMs), Bayesian networks, or latent variable structural equation modeling.

Instead of evaluating individual transactions in isolation, AQFM models the system as a dynamic state-space. If is the unobserved vector of true fraud risk parameters at time t, and is the vector of observed environmental telemetry and sparse loss signals, the modeling layer estimates the conditional probability:

This allows the risk engineering team to calculate confidence intervals around the expected risk mass, identifying when the variance of the underlying system is expanding dangerously.

By executing continuous latent state estimation, the modeling layer determines the structural parameters of the risk PDF—specifically focusing on its variance and tail behavior. If the model detects that the right tail of the distribution is growing fatter (indicating a heightened probability of a coordinated, multi-million dollar exploit wave), it signals an immediate anomaly. This holds true even if the current median loss realization sits comfortably below the quarterly KPI target. Modeling ensures that the business quantifies its exposure to what could happen based on structural design, rather than what has happened based on historical luck.

DECIDE: Distributional Control & The Friction Fallacy

In a conventional fraud shop, automated decisions are optimized for point estimates: minimize expected loss while maintaining a specified transaction conversion threshold. The outcome is a series of hard-coded block/allow rules or rigid score cutoffs. AQFM rejects this narrow framing, re-imagining the decision layer as a problem of stochastic control. The fundamental objective of any decision, control, or policy intervention is to act as a mathematical transformer on the probability density function itself.

When an AQFM risk architect deploys a control, they are not merely trying to block “Transaction X”; they are trying to shape the geometry of the risk distribution. Specifically, decisions should be designed to compress the variance, thin out the right tail, and shift the overall mass of the distribution as close to zero as possible. This approach prevents catastrophic black swan events—those highly coordinated, low-frequency but hyper-high-severity attacks that can bankrupt a high-growth fintech platform in a single weekend.

The Friction Fallacy: A critical point of failure in modern risk design is the indiscriminate application of friction (e.g., blanket CAPTCHAs, manual reviews, or aggressive KYC re-verification). Under AQFM, friction without structural modification is recognized as operational malpractice.

Friction often acts merely as a volume filter. It reduces total transaction velocity, thereby reducing the absolute count of realized losses, but it leaves the parameters of the latent risk distribution unchanged. The underlying vulnerability remains wide open; the adversary simply pauses or refines their scripts. The moment growth pressures force the business to remove the friction, losses surge immediately. True AQFM decisions change the system architecture to eliminate the vulnerability entirely, altering the risk distribution permanently.

Distributional control means that if a platform discovers a vulnerability in its instant-payout mechanism, a legacy decision would be to apply a strict 48-hour manual review hold on all payouts—inflicting massive friction on legitimate users. An AQFM decision, by contrast, dynamically modifies the payout availability function based on the latent risk state. It might compress the maximum instant-payout ceiling dynamically for higher-variance cohorts while maintaining a frictionless path for the low-variance mass, effectively slicing off the catastrophic right tail of the risk distribution without degrading the macro-conversion profile of the platform.

The final verb of the AQFM framework embeds a critical truth into the system design: fraud mitigation is a dynamic, adversarial game. Unlike credit risk, where default probabilities are governed by macroeconomic trends and structural financial behaviors that evolve slowly over years, fraud risk is highly non-stationary. You are not predicting natural phenomena like the weather; you are locked in a continuous tactical duel with an intelligent, well-capitalized human adversary who reads your API documentation, tests your defenses, and responds fluidly to your controls.

ADAPT: Managing Adversarial Non-Stationarity

Every single decision and control implemented by a risk team updates the opponent’s strategy profile. If you build a highly effective biometric defense at the account creation layer, the adversary does not capitulate; they pivot upstream to purchase pre-warmed accounts on the dark web, or they move downstream to execute social engineering scams on existing high-value users. Consequently, any risk distribution you successfully shape will naturally begin to degrade, widen, and shift over time as the adversary adapts to your current layout.

The Adapt layer of AQFM creates an automated, continuous feedback loop between operational outcomes and model parameter tuning. It treats the controls themselves as experiments that generate new signal telemetry. Through techniques such as continuous shadow testing, champion-challenger modeling, and automated reinforcement learning loops, the Adapt layer monitors for signs of control degradation. It detects when the adversary has bypassed a defense long before that bypass manifests as an explicit financial loss line, automatically triggering a recalculation of the latent risk state and prompting a reconfiguration of the Measure and Model layers.

Operationalizing AQFM: The Closed-Loop Architecture

The true power of the AQFM framework manifests when these four verbs cease to operate as isolated, siloed functions and instead fuse into a unified, closed-loop cybernetic system. The output of one verb serves directly as the fuel for the next, establishing a continuous cycle of risk engineering:

To implement AQFM in an enterprise environment, risk leaders must break down the historical walls separating risk policy analysts, data scientists, and core product engineers. The team must operate as a singular unit dedicated to managing the probability distribution. KPI matrices must shift: teams should no longer be evaluated solely on the historical net loss rate or transaction approval rates. Instead, they should be measured on risk-variance compression, the speed of latent anomaly detection, and the long-term mathematical stability of the platform’s conversion-to-risk efficiency frontier.

Conclusion: From Firefighting to Risk Engineering

The traditional model of fraud management is fundamentally unsustainable. In an era of instant payment rails, generative AI-driven identity synthesis, and highly automated cybercrime infrastructure, the legacy cycle of reacting to historical chargebacks ensures that an enterprise is always one step behind the adversary. It leaves organizations exposed to catastrophic tail risk while forcing them to inflict blunt, conversion-killing friction on their legitimate customer base.

AQFM provides the paradigm shift required for modern digital commerce. By decoupling realized losses from latent risk, and framing the operational mandate around the precise execution of measuring topology, modeling latent states, deciding on distributional controls, and adapting to non-stationary adversaries, AQFM transforms risk management from a chaotic cost-center firefighting unit into a predictable, mathematically rigorous engineering discipline. It allows enterprises to stop looking at the rearview mirror and finally take complete control of the statistical path ahead.

Leave a Reply